Content

Focus on long-term growth

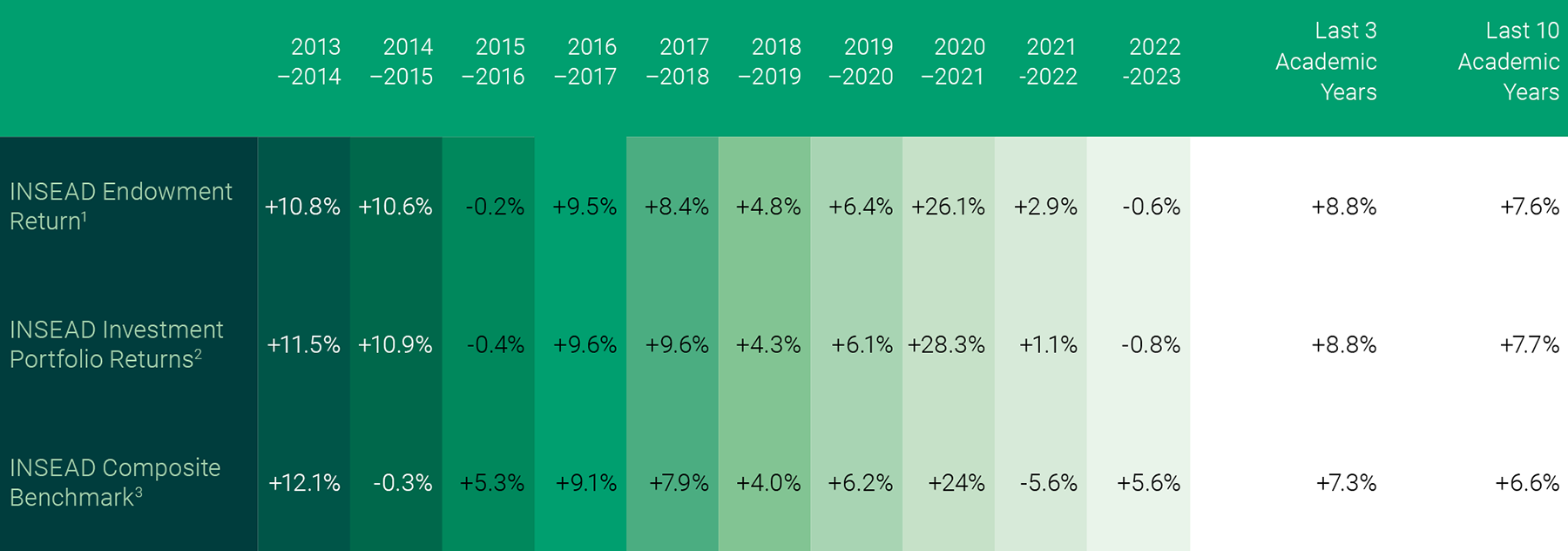

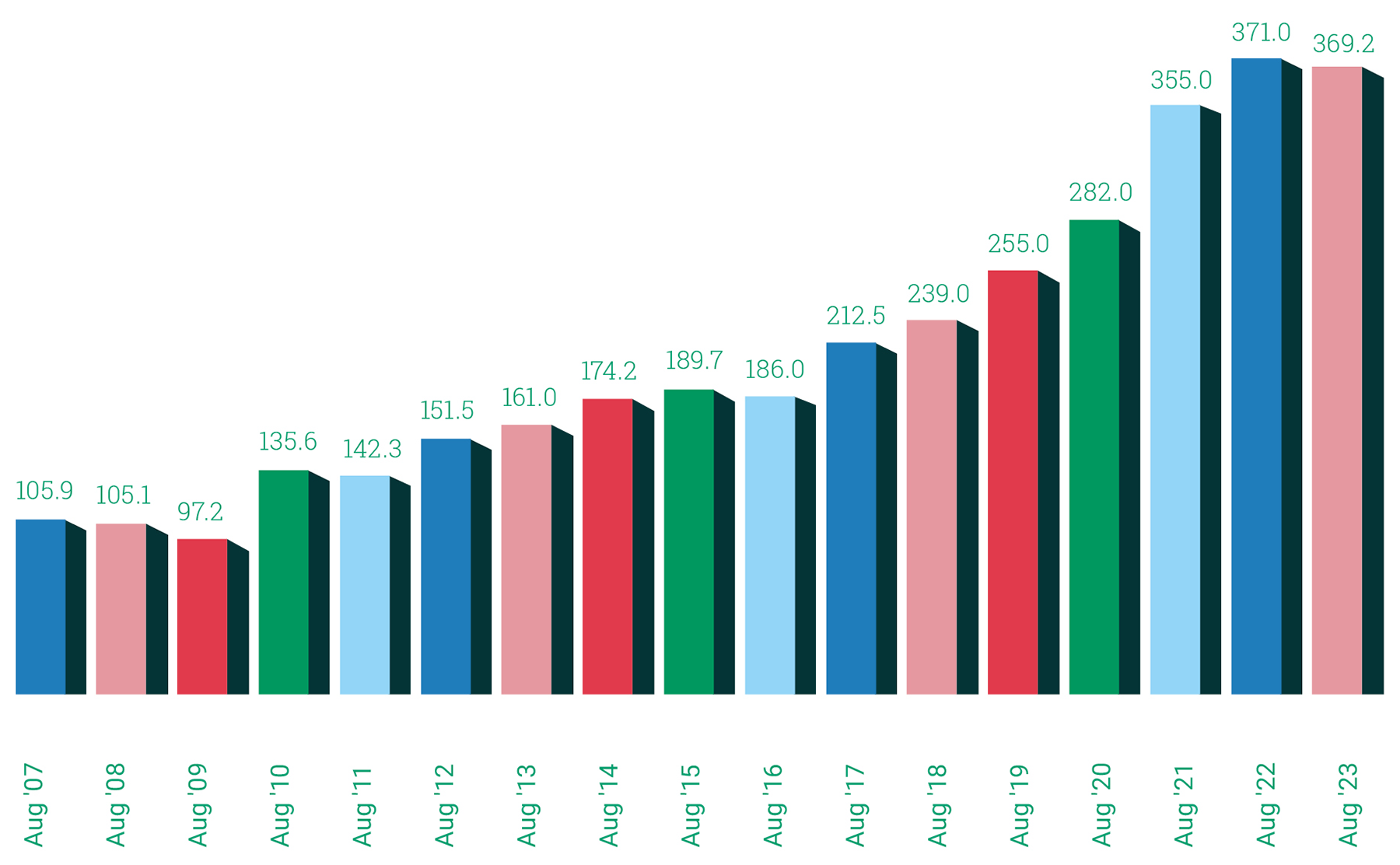

The Endowment’s investment strategy is firmly anchored in maximising long-term risk-adjusted returns, with a strong emphasis on integrating ESG factors into our decision making. We are guided by the following principles:

- High equity exposure, aligned with our long-term outlook;

- Diversified asset classes, including a significant allocation to private markets where we see the greatest potential for outperformance;

- Selective asset-manager engagement, focused on the most skilled in each asset class;

- Sustainable investment practices, reflecting INSEAD’s commitment to business as a force for good.

Portfolio allocation

Private markets (40%): This includes private equity, real estate and private debt, targeting the illiquidity premium typically ranging between +3% and +5%. Our private-market investments are diverse, encompassing venture capital in early-stage tech firms, private equity in lower middle-market companies, European real estate and senior loans to private businesses. We have continued to ramp up our commitments to private debt and to buyout managers with a proven ability to bring value-enhancing operational improvements to their portfolio companies.

Public equities (38%): This, combined with our private-market portfolio, forms the core of our long-term, return-generating strategy. Our public equity investments include a mix of actively managed long-only and long-short funds, alongside passive index trackers.

Credit investments (15%): To capitalise on higher yields, we have increased our allocation to credit investments across both public and private strategies.

Hedge funds and inflation-linked bonds (7%): Our investment in absolute-return hedge funds is designed to yield returns with minimal correlation to traditional assets and thrive in higher volatility. Inflation-linked government bonds offer additional protection against unexpected inflation spikes.

Investing in partnership

While the Endowment Management Committee holds direct responsibility for our investments, our portfolio is skilfully managed by Partners Capital, our advisors since 2007. We extend our gratitude to Partners Capital for their support in fostering the long-term growth of our Endowment over the last remarkable decade in INSEAD’s history.